Employer of Record Poland: The Complete Guide for Foreign Companies Hiring in 2025 and 2026

Setting up a legal entity in Poland to hire local talent can take 2–4 months and cost up to PLN 294,000 (approximately $73,500 USD) in legal, tax, and payroll setup fees. Meanwhile, the global Employer of Record market is projected to grow from $5 billion in 2026 to $19.8 billion by 2036 at a 14.8% compound annual growth rate according to industry research from Rise and Employsome. This explosive growth signals a fundamental shift in how companies approach international expansion and global talent acquisition.

Poland has emerged as one of Europe’s most attractive destinations for tech talent acquisition. With over 400,000 professional software developers, competitive salary bands 40–60% below Western European levels, and strong STEM education pipelines, the country offers foreign companies access to high-quality engineering talent without the premium costs of London, Munich, or Amsterdam. Major global technology companies including Google, Microsoft, Amazon, and IBM have established significant development centers in Poland, validating the country’s position as a premier technology hub. Yet navigating Polish labor law, social security contributions, and compliance requirements presents significant challenges for companies without local expertise.

This comprehensive guide covers everything you need to know about using an Employer of Record (EOR) in Poland: how it works, what compliance obligations it handles, how costs compare to entity setup, when it makes sense for your business, and how to select the right provider. Whether you are a startup testing the Polish market, a scaleup building a distributed team, or an enterprise scaling your Central and Eastern European engineering hub, this article provides the data, frameworks, and actionable insights to make an informed decision.

What Is an Employer of Record (EOR) in Poland?

An Employer of Record in Poland is a licensed local entity that hires workers on your behalf, assuming the full legal role of “pracodawca” (employer) under the Polish Labor Code (Kodeks Pracy). Your company manages day-to-day work—projects, performance, and culture—while the EOR handles all legal and administrative employment obligations. This arrangement is sometimes referred to as a Professional Employer Organization (PEO) in other jurisdictions, though the EOR term is more commonly used for international employment arrangements.

The EOR model creates a three-party relationship: your company directs the work and defines deliverables, the EOR serves as the legal employer for tax and compliance purposes, and the employee performs their duties under your operational management. This structure allows foreign companies to hire Polish talent without establishing a local subsidiary, branch office, or representative office. The EOR becomes the employer of record for tax authorities, social security institutions, and labor inspectors, while your company maintains full control over the employee’s work activities, projects, and performance management.

Core Services Provided by a Polish EOR

A comprehensive EOR service in Poland typically includes the following components:

- Employment contracts: Drafting and signing Polish-language employment contracts compliant with the Labor Code, including fixed-term (umowa na czas określony) and indefinite (umowa na czas nieokreślony) contracts with proper probation periods. The EOR ensures all mandatory clauses are included and that contracts comply with current labor regulations.

- ZUS registration: Registering employees with the Social Insurance Institution (Zakład Ubezpieczeń Społecznych) for pension, disability, sickness, and accident insurance coverage. This includes obtaining ZUS numbers and ensuring proper classification of employment.

- Payroll processing: Calculating gross-to-net pay, withholding personal income tax (PIT), remitting social security contributions, and filing monthly Płatnik reports through Poland’s official payroll portal. The EOR handles all calculations, ensuring accuracy and compliance with current rates.

- Tax compliance: Managing advance PIT payments, annual PIT-11 certificates for employees, and IFT-1/11 filings for foreign employers. The EOR ensures all tax obligations are met and that employees receive proper documentation for their annual tax returns.

- Benefits administration: Handling statutory benefits including vacation leave, sick pay, maternity/paternity/parental leave, and PPK auto-enrollment and management. The EOR tracks entitlements and ensures employees receive all legally mandated benefits.

- Labor Fund and FGŚP: Calculating and remitting contributions to the Labor Fund (Fundusz Pracy) and Guaranteed Employee Benefits Fund (Fundusz Gwarantowanych Świadczeń Pracowniczych). These mandatory contributions support employment programs and protect workers in case of employer insolvency.

- Termination management: Processing notice periods, severance calculations, and mutual termination agreements in strict compliance with Polish dismissal protections. Polish labor law heavily favors employees in termination scenarios, making expert handling essential.

- GDPR compliance: Ensuring all employee data processing meets EU General Data Protection Regulation requirements. This includes maintaining proper consent records, implementing security measures, and respecting employee data rights.

- Work permits and visas: Supporting visa applications and work permit sponsorship for non-EU nationals. While EU citizens can work freely in Poland, non-EU nationals require proper documentation.

The Legal Framework: Polish Labor Code Essentials

Poland’s employment law is governed by the Labor Code of June 26, 1974, supplemented by EU directives, international labor agreements, and numerous regulations issued by the Council of Ministers. The Labor Code establishes strict protections for employees, making compliance complex for foreign employers unfamiliar with local nuances. Understanding these requirements is essential for any company hiring in Poland, whether directly or through an EOR.

Key legal requirements that every employer in Poland must follow include:

- Written employment contracts must be signed no later than the first working day; failure to provide a written contract results in presumption of an indefinite contract. This means that if you allow an employee to start work without a signed contract, they are automatically considered to have an indefinite-term contract with full protections.

- Probation periods cannot exceed three months and must be explicitly agreed in writing. The probation period allows both parties to assess fit, but strict rules govern its duration and termination during this period.

- Standard work week is 40 hours over five days, with overtime compensated at 150% (200% for night work, Sundays, and holidays). Polish law strictly regulates working time and requires accurate record-keeping.

- Minimum wage is PLN 4,666 gross monthly in 2025, increasing to PLN 4,806 in 2026. This represents a significant increase from previous years as the government works to boost incomes.

- Minimum hourly rate is PLN 30.50 in 2025, rising to PLN 31.40 in 2026. This applies to civil law contracts and part-time arrangements.

- Employees with under 10 years of work experience receive 20 days annual leave; those with 10+ years receive 26 days. Leave entitlement increases with seniority and is strictly protected.

- Employers with 20+ employees must auto-enroll eligible staff in Employee Capital Plans (PPK). This auto-enrollment retirement savings program requires careful administration.

- 13 public holidays per year; if a holiday falls on a Saturday, employers must grant an additional paid day off. This “day off in lieu” requirement catches many foreign employers by surprise.

Violations of these regulations can result in fines from the State Labour Inspectorate (Państwowa Inspekcja Pracy), back-pay obligations, and significant reputational damage. Employee disputes frequently favor the worker in Polish courts, making proactive compliance essential. The Inspectorate actively conducts workplace audits and can impose penalties for even technical violations.

Why Poland for Tech Hiring?

Poland has established itself as a premier destination for technology talent in Central and Eastern Europe. The country offers several compelling advantages that make it attractive for foreign companies seeking to build engineering teams:

- Deep talent pool: Over 400,000 professional software developers, with approximately 75,000 IT graduates entering the market annually. Polish universities produce more STEM graduates per capita than most European countries.

- Strong technical education: Polish universities consistently rank among Europe’s best for computer science and engineering, with institutions like Warsaw University of Technology, AGH University of Krakow, Wrocław University of Science and Technology, and Jagiellonian University producing world-class engineers. Many Polish developers hold advanced degrees and certifications.

- Competitive costs: Developer salaries 40–60% lower than Western Europe and 70–80% lower than Silicon Valley. A senior developer in Poland might earn PLN 20,000–30,000 monthly (€4,500–€6,800), compared to €8,000–€12,000 in Germany or $150,000–$200,000 in the US.

- EU membership: Full access to the European single market, freedom of movement for EU citizens, and GDPR alignment. This provides legal certainty and simplifies data handling for EU-based companies.

- Cultural compatibility: High English proficiency (ranked 13th globally in EF English Proficiency Index 2024), Western work culture, and strong work ethic. Polish developers are known for their problem-solving skills and dedication.

- Time zone advantage: Central European Time (CET) enables real-time collaboration with Western Europe and significant overlap with US East Coast. This is ideal for distributed teams requiring synchronous communication.

- Thriving tech ecosystem: Major hubs in Warsaw, Kraków, Wrocław, Gdańsk, and Łódź with active startup communities, tech meetups, and established global tech presence. Google, Microsoft, Amazon, IBM, and Oracle all have significant operations in Poland.

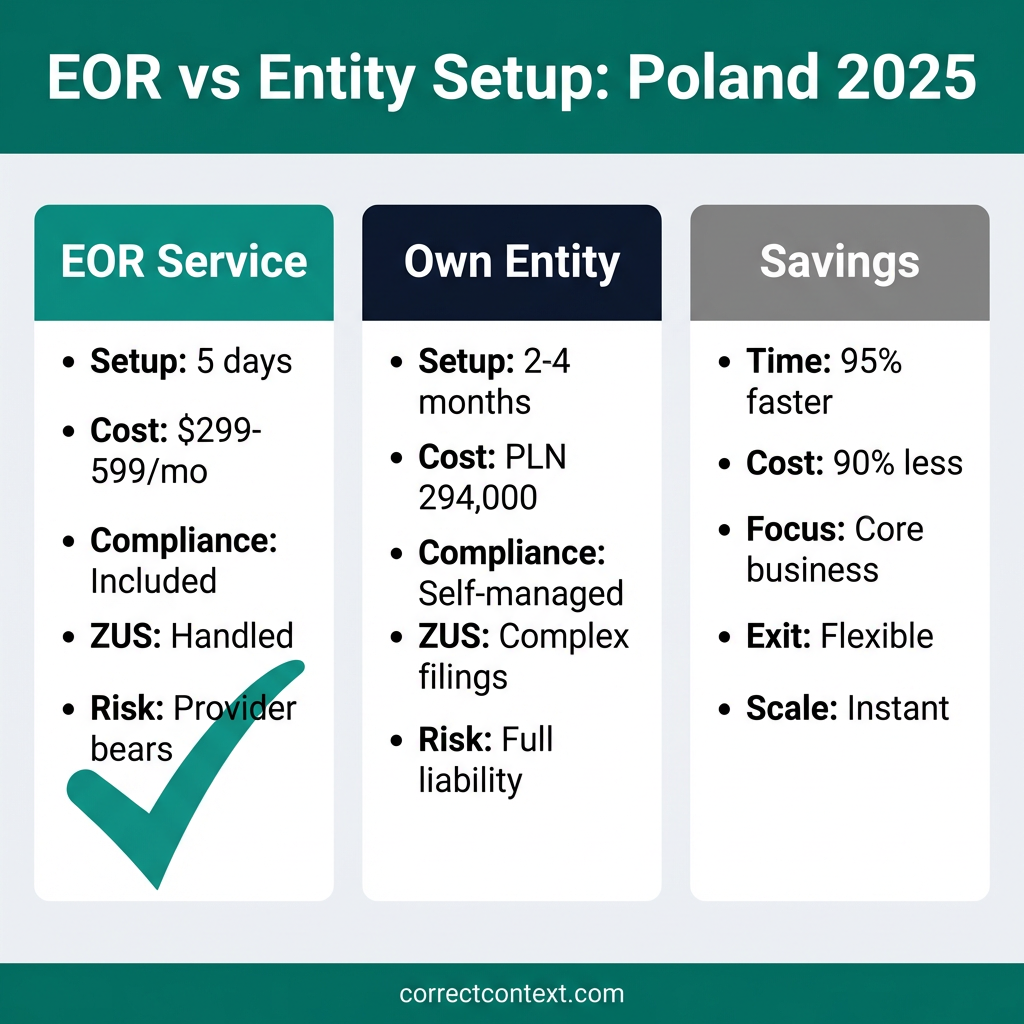

EOR vs. Entity Setup: A Comprehensive Cost Comparison

The decision between using an EOR and establishing your own Polish entity hinges on multiple factors: time to hire, upfront investment, ongoing compliance burden, strategic flexibility, and long-term commitment to the market. Here is a detailed breakdown of the true costs involved in each approach.

One-Time Setup Costs

Establishing a legal entity in Poland requires significant upfront investment in legal services, registration fees, and operational setup. These costs are incurred before hiring your first employee and represent sunk costs if the market entry does not succeed.

| Cost Component | Own Entity (PLN) | Own Entity (USD) | EOR |

|---|---|---|---|

| Legal fees (incorporation, notary, contracts) | 15,000 – 25,000 | $3,750 – $6,250 | $0 |

| Share capital (minimum for sp. z o.o.) | 5,000 | $1,250 | $0 |

| REGON statistical number registration | 0 (free) | $0 | $0 |

| NIP tax identification number | 0 (free) | $0 | $0 |

| VAT registration (if applicable) | 0 (free) | $0 | $0 |

| Bank account setup and initial deposits | 0 – 500 | $0 – $125 | $0 |

| Accounting and payroll system setup | 5,000 – 10,000 | $1,250 – $2,500 | $0 |

| Office lease deposit (if physical presence) | 20,000 – 50,000 | $5,000 – $12,500 | $0 |

| Initial legal and compliance consultation | 10,000 – 20,000 | $2,500 – $5,000 | $0 |

| Translation and document certification | 2,000 – 5,000 | $500 – $1,250 | $0 |

| Total One-Time Costs | 57,000 – 115,500 | $14,250 – $28,875 | $0 |

Source: Deel EOR Poland Guide (2026), Polish Accounting Office estimates (2025).

Annual Operating Costs (Per Employee)

Beyond setup costs, operating your own entity incurs ongoing expenses for accounting, legal compliance, HR administration, and office overhead. These costs scale with headcount but remain significant even for small teams.

| Cost Component | Own Entity (PLN/year) | Own Entity (USD/year) | EOR (typical) |

|---|---|---|---|

| Accounting and bookkeeping services | 12,000 – 24,000 | $3,000 – $6,000 | Included |

| Legal compliance retainer | 6,000 – 12,000 | $1,500 – $3,000 | Included |

| Payroll administration and ZUS filings | 3,600 – 6,000 | $900 – $1,500 | Included |

| Tax advisory and filing services | 4,800 – 9,600 | $1,200 – $2,400 | Included |

| HR administration (contracts, policies) | 12,000 – 24,000 | $3,000 – $6,000 | Included |

| HRIS and payroll software licenses | 3,600 – 7,200 | $900 – $1,800 | Included |

| Office overhead (pro-rated per employee) | 24,000 – 60,000 | $6,000 – $15,000 | $0 |

| Audit and compliance monitoring | 3,000 – 6,000 | $750 – $1,500 | Included |

| EOR management fee | N/A | N/A | $3,588 – $7,188 |

| Total Annual Costs | 69,000 – 148,800 | $17,250 – $37,200 | $3,588 – $7,188 |

Note: EOR fees typically range from $299 to $599 per employee per month, depending on provider, service level, and volume discounts. Some providers offer lower rates for higher volumes or longer commitments.

Time-to-Hire Comparison

Beyond direct costs, time is a critical competitive factor. Setting up a Polish entity typically requires:

- Weeks 1–2: Legal consultation, documentation preparation, and engagement of local advisors. This phase involves selecting a law firm, defining corporate structure, and preparing incorporation documents.

- Weeks 3–6: Notary appointments, company registration with National Court Register (KRS), and obtaining KRS number. The notary must authenticate signatures and articles of association.

- Weeks 7–10: Tax identification (NIP), statistical number (REGON), and VAT registration with tax authorities. These registrations are required before the company can conduct business.

- Weeks 11–14: Corporate bank account opening, payroll system configuration, and ZUS employer registration. Banks require extensive documentation for corporate accounts.

- Week 15+: First employee onboarding, contract execution, and initial payroll run. Only at this point can hiring begin.

By contrast, an EOR can onboard a Polish employee in 5–10 business days. This 95% reduction in time-to-hire allows companies to seize market opportunities, respond to competitive talent situations, secure candidates who have multiple offers, and iterate quickly on product-market fit without administrative delays.

Hidden Costs of Entity Setup

Several costs are often overlooked when calculating the true expense of establishing a Polish entity:

- Management time: Senior leadership attention diverted to legal setup, compliance reviews, and vendor selection. This opportunity cost can be significant for startups and scaleups.

- Compliance risk: Penalties for errors in ZUS filings, tax calculations, or contract terms can reach tens of thousands of PLN. Even innocent mistakes can result in fines.

- Exit costs: Dissolving a Polish entity requires formal liquidation procedures, creditor notifications, and regulatory filings—costing PLN 10,000–30,000 and taking 6–12 months. This creates a significant barrier to exiting the market.

- Opportunity cost: Delayed market entry while competitors capture talent and customers. In fast-moving markets, months of delay can mean losing the best candidates to competitors.

When Entity Setup Makes Sense

Despite the higher costs and longer setup time, establishing your own Polish entity may be preferable when specific conditions are met:

- You plan to hire 15+ employees in Poland within 18 months, achieving economies of scale that offset fixed compliance costs. At this scale, per-employee costs of entity operation may fall below EOR fees.

- You require full control over IP ownership, contractual terms, and employment policies. Some companies have specific requirements that standard EOR arrangements cannot accommodate.

- You intend to establish a significant physical presence (dedicated office, R&D center, or regional headquarters). A local entity provides the legal framework for substantial operations.

- You have existing European operations and want to consolidate legal structures under a single EU entity. This can simplify corporate governance and reporting.

- You are pursuing government grants, EU funding, or tax incentives requiring local entity registration. Many incentive programs require a registered Polish entity.

- You operate in a highly regulated industry requiring direct regulatory relationships. Financial services, healthcare, and other regulated sectors may need direct licensing.

For most companies testing the Polish market, hiring 1–10 employees, or seeking flexibility to scale up or down, the EOR model provides superior speed, cost efficiency, and risk management.

Understanding Poland’s Employer Cost Structure

Poland’s employment costs extend significantly beyond gross salary. Employers must budget for mandatory social contributions, insurance, and statutory funds. Understanding these costs is essential for accurate financial planning and competitive compensation benchmarking.

Social Security Contributions (ZUS)

The Social Insurance Institution (Zakład Ubezpieczeń Społecznych, or ZUS) administers Poland’s comprehensive social security system. Employer contributions fund retirement pensions, disability benefits, and workplace accident compensation.

| Contribution Type | Employer Rate | Employee Rate | Purpose |

|---|---|---|---|

| Pension insurance (emerytalne) | 9.76% | 9.76% | Retirement benefits |

| Disability insurance (rentowe) | 6.50% | 1.50% | Disability pensions and benefits |

| Accident insurance (wypadkowe) | 0.67% – 3.33% | 0% | Workplace injury compensation |

| Sickness insurance (chorobowe) | 0% | 2.45% | Sick leave benefits |

| Health insurance (zdrowotne) | 0% | 9% | Public healthcare access |

| Total ZUS (employer) | ~16.93% – 19.59% | — | Social insurance coverage |

The accident insurance rate varies by industry classification and company safety record, with most technology companies paying the minimum 0.67%. High-risk industries such as construction or manufacturing may pay up to 3.33%.

Labor Fund (Fundusz Pracy) and FGŚP

Beyond ZUS, employers must contribute to two additional statutory funds:

- Labor Fund (Fundusz Pracy, FP): 2.45% of gross salary—supports employment programs, vocational training, countering unemployment, and financing the Guaranteed Employee Benefits Fund. This fund finances active labor market policies.

- Guaranteed Employee Benefits Fund (Fundusz Gwarantowanych Świadczeń Pracowniczych, FGŚP): 0.10% of gross salary—protects employees when employers become insolvent, ensuring payment of unpaid wages, severance, and other benefits. This provides a safety net for workers.

Employee Capital Plans (PPK)

Introduced in 2019 and fully implemented by 2021, PPK (Pracownicze Plany Kapitałowe) is Poland’s auto-enrollment retirement savings program designed to supplement the state pension system. Employers with 20 or more staff members must automatically enroll eligible employees.

PPK contribution structure:

- Employer contribution: 1.5% of gross salary (mandatory minimum), with option to contribute up to 4.0% total. Many employers choose to contribute more to enhance their benefits package.

- Employee contribution: 2.0% of gross salary (mandatory minimum), with option to contribute up to 4.0% total. Employees can also make additional voluntary contributions.

- State contribution: PLN 250 annual welcome payment for new enrollees plus PLN 240 annual top-up. This government contribution incentivizes participation.

- Additional employee contribution: Employees may voluntarily contribute up to additional 2.0% beyond the base contribution.

Eligibility and enrollment rules:

- Employees aged 18–54 are automatically enrolled but may opt out within a specified window

- Employees aged 55–70 may voluntarily join but are not auto-enrolled

- Employees under 18 or over 70 are not eligible

- Non-compliance with PPK obligations can result in fines up to PLN 1,000,000

Total Cost of Employment Example

For a mid-level software developer earning PLN 15,000 gross monthly (PLN 180,000 annually), the total employer cost breaks down as follows:

| Cost Component | Monthly (PLN) | Annual (PLN) | Notes |

|---|---|---|---|

| Gross salary | 15,000 | 180,000 | Base compensation |

| ZUS employer contributions (~17.5%) | 2,625 | 31,500 | Pension + disability + accident |

| Labor Fund FP (2.45%) | 368 | 4,410 | Mandatory employment fund |

| FGŚP (0.10%) | 15 | 180 | Insolvency protection |

| PPK employer (1.5%) | 225 | 2,700 | Auto-enrolled pension |

| Total Employer Cost | 18,233 | 218,790 | Full cost of employment |

| Effective Cost Beyond Salary | 21.6% | ||

This means a PLN 15,000 gross salary actually costs the employer approximately PLN 18,233 monthly when all statutory contributions are included. For budgeting purposes, employers should plan for 21–23% additional cost beyond gross salary.

2025–2026 Minimum Wage Changes

Poland’s minimum wage has increased significantly in recent years as part of government policy to boost incomes. Current and upcoming rates:

| Period | Monthly Gross | Hourly Rate |

|---|---|---|

| 2025 | PLN 4,666 | PLN 30.50 |

| 2026 (from January 1) | PLN 4,806 | PLN 31.40 |

For a minimum wage employee in 2026, the total employer cost including all contributions will exceed PLN 5,800 monthly. Companies employing significant numbers of minimum wage workers should budget for these increases.

The EOR Hiring Process: Step-by-Step

Working with an EOR follows a standardized process designed for speed, compliance, and minimal administrative burden on the client company. Here is what to expect when hiring through a Polish EOR.

Phase 1: EOR Selection and Agreement (Days 1–2)

Step 1: Choose an EOR with a wholly-owned Polish entity. Verify that the provider directly controls its local entity rather than outsourcing to a third-party partner. Direct ownership ensures clearer accountability, faster issue resolution, immediate contract signing under the provider’s REGON and NIP numbers, and single-point-of-contact service.

Key questions to ask potential EOR providers:

- Do you own your Polish entity directly, or do you partner with a local provider?

- What is your average time-to-hire for Polish employees?

- How do you handle ZUS filings and Płatnik reporting?

- What is included in your management fee, and what costs extra?

- How do you manage PPK auto-enrollment and employee opt-outs?

- What is your process for termination and severance calculations?

- Can you provide references from companies in our industry?

Step 2: Request a transparent quote. A quality EOR quote itemizes all costs: gross salary, statutory employer contributions (ZUS, FP, FGŚP, PPK), and the management fee. Avoid providers with hidden markups, vague pricing, or unexpected charges for standard services.

Step 3: Sign the EOR service agreement. This master contract establishes the three-party relationship, defines responsibilities and liability allocation, specifies service levels and response times, and outlines termination conditions for both parties.

Phase 2: Candidate Selection and Verification (Days 2–3)

Step 4: Submit role requirements. Provide the EOR with detailed job descriptions, compensation ranges, required qualifications, and candidate profiles. The EOR reviews offers for compliance with Polish labor law, including minimum wage requirements, statutory benefits, and working time regulations.

Step 5: Verify right-to-work status. Confirm the candidate’s eligibility to work in Poland. EU citizens have automatic right to work, while non-EU nationals require valid work permits. Many EORs offer visa sponsorship and work permit application services for an additional fee.

Step 6: Draft the employment contract. The EOR generates a compliant Polish-language employment contract (umowa o pracę) including all legally required clauses: job title and description, compensation and payment terms, working hours and location, probation period (maximum 3 months), notice periods by tenure, termination conditions, and data protection provisions. Bilingual contracts are typically available for foreign employers.

Phase 3: Onboarding and Registration (Days 3–5)

Step 7: Contract execution. The candidate signs the employment contract with the EOR as the legal employer. Your company signs a separate service agreement or work order defining the management relationship, deliverables, and commercial terms.

Step 8: ZUS and tax registration. The EOR registers the employee with ZUS for social insurance coverage (pension, disability, sickness, accident), obtains tax identification, and establishes monthly Płatnik reporting obligations.

Step 9: PPK enrollment. For companies with 20+ employees, the EOR auto-enrolls eligible staff in Employee Capital Plans, processes opt-out requests from employees who decline participation, and manages ongoing contribution calculations.

Step 10: First payroll setup. The EOR configures payroll parameters, establishes payment schedules (typically monthly, by the 10th or 28th of the month), and ensures all statutory withholdings are calculated correctly.

Phase 4: Ongoing Management

Once the employee starts work, the EOR assumes responsibility for:

- Monthly payroll processing: Calculating gross-to-net, withholding PIT, remitting ZUS contributions, and disbursing salary by the contractually agreed date

- Płatnik filings: Submitting monthly ZUS and tax reports by the 15th of the following month

- Annual tax certificates: Issuing PIT-11 forms to employees and IFT-1/11 filings for foreign employers by end of February

- Leave management: Tracking vacation entitlement (20–26 days annually), processing sick leave (up to 33 days employer-paid), and administering maternity/paternity/parental leave

- Benefits administration: Managing optional benefits such as private medical insurance, meal vouchers (bona), gym memberships, and equipment provisioning

- Termination processing: Calculating notice periods (2 weeks to 3 months), severance pay for redundancies, and final settlements

- Compliance monitoring: Tracking regulatory changes and implementing adjustments to maintain continuous compliance

Compliance Risks and How EOR Mitigates Them

Poland’s labor law enforcement is stringent, and non-compliance carries significant financial and reputational penalties. An EOR acts as a compliance shield, absorbing legal risk and ensuring adherence to complex, frequently changing regulations.

Misclassification Risk

Polish courts and labor inspectors routinely reclassify B2B contractors (self-employed) as employees when the working relationship exhibits characteristics of employment. Factors that trigger reclassification include:

- Fixed working hours determined by the company

- Subordination to company management and supervision

- Use of company equipment, software, and resources

- Integration into company operations and teams

- Exclusive service to one client

- Performance of core business activities rather than advisory services

Consequences of misclassification can be severe:

- Retroactive ZUS contributions for the entire engagement period (employee + employer portions plus penalties)

- Back-pay for vacation leave, sick leave, and other statutory benefits the contractor was denied

- Fines from the State Labour Inspectorate ranging from PLN 1,000 to PLN 30,000 per violation

- Criminal liability for intentional tax and social security evasion

- Reputational damage making future hiring in Poland more difficult

An EOR eliminates misclassification risk entirely by establishing a proper employment relationship from day one, with the EOR as the legal employer and the worker receiving all statutory protections and benefits.

Termination and Severance Complexity

Polish employment law heavily favors employees in termination scenarios, with strict procedural requirements and substantial financial obligations. Notice periods depend on tenure and contract type:

| Tenure | Notice Period |

|---|---|

| Probation (up to 3 months) | 3 days to 2 weeks |

| Less than 6 months | 2 weeks |

| 6 months to 3 years | 1 month |

| Over 3 years | 3 months |

Severance pay is mandatory for terminations due to reasons unrelated to the employee (redundancy, restructuring, position elimination):

- Up to 2 years tenure: No severance required

- 2–8 years tenure: 1 month salary

- 8+ years tenure: 2 months salary

Wrongful termination claims can result in reinstatement orders, compensation for lost wages during the dispute period, and damage to employer reputation. EORs manage terminations through mutual agreements when possible, following strict procedural requirements to minimize legal exposure.

GDPR and Data Protection Compliance

As an EU member state, Poland enforces the General Data Protection Regulation (GDPR) strictly, with additional protections under Polish data protection law. Employee data processing requirements include:

- Lawful basis for processing (typically employment contract necessity or legal obligation)

- Proper consent mechanisms for sensitive data processing

- Data minimization and purpose limitation principles

- Security measures appropriate to risk level

- Data retention limits and secure deletion procedures

- Employee rights to access, rectification, erasure, and portability

Companies with 250+ employees must appoint a Data Protection Officer (DPO). Data breaches can result in fines up to €20 million or 4% of global annual turnover.

EORs maintain GDPR-compliant systems, EU-based data centers, standardized privacy policies, and trained personnel—reducing compliance burden and liability for foreign employers.

2025–2026 Regulatory Changes

Several regulatory changes affect Polish employers in 2025 and 2026, requiring ongoing monitoring and adjustment:

- Minimum wage increases: PLN 4,666 monthly (2025) → PLN 4,806 (2026), with further increases expected as Poland converges toward EU averages

- Length of service calculation: From January 2026, periods worked under B2B contracts and mandate contracts (umowa zlecenie) count toward employment tenure for vacation entitlements and other seniority-based benefits

- Enhanced Labour Inspectorate powers: New authority to audit B2B relationships, reclassify contractors, and impose immediate corrective measures

- Holiday benefit obligations: Companies with under 50 employees must pay holiday benefits; those with 50+ must establish Company Social Benefit Funds (ZFŚS)

EORs monitor these changes and implement adjustments automatically, ensuring continuous compliance without requiring client intervention.

Key Takeaways

- Speed advantage: EOR enables hiring in 5–10 days versus 2–4 months for entity setup, allowing companies to capture market opportunities quickly

- Cost efficiency: EOR management fees ($299–599/employee/month) are significantly lower than entity setup costs (PLN 294,000+), especially for small teams

- Compliance coverage: EORs handle ZUS, PIT, PPK, Labor Fund, FGŚP, and GDPR obligations, eliminating compliance burden

- Risk mitigation: EORs absorb liability for misclassification, termination disputes, and regulatory violations

- Total employer costs: Budget approximately 21–23% above gross salary for mandatory contributions in Poland

- Market growth: The global EOR market is growing at 14.8% CAGR, reflecting permanent shifts toward distributed work and global hiring

- Entity threshold: Consider establishing your own entity when hiring 15+ employees in Poland with long-term commitment

Frequently Asked Questions

How fast can I hire an employee in Poland using an EOR?

Most EORs can onboard a Polish employee in 5–10 business days, compared to 2–4 months required to establish your own legal entity. This includes contract drafting, ZUS registration, and first payroll setup.

What is the minimum wage in Poland for 2025 and 2026?

The minimum wage in Poland is PLN 4,666 gross per month (PLN 30.50 hourly) in 2025, increasing to PLN 4,806 gross per month (PLN 31.40 hourly) from January 1, 2026.

Do I need a Polish bank account to pay employees through an EOR?

No. The EOR handles all local payments, including salary disbursements and tax remittances. You pay the EOR in your home currency according to invoicing terms.

What employment contract does an EOR use in Poland?

EORs issue compliant Polish-language employment contracts (umowa o pracę) that include all legally required clauses: job description, compensation, working hours, probation period, notice periods, and data protection provisions. Bilingual versions are typically available.

Does an EOR manage Polish payroll taxes and social security?

Yes. EORs calculate, withhold, and remit all required PIT (personal income tax), ZUS (social security contributions), and PPK (pension) contributions via Poland’s Płatnik system. Monthly filings are due by the 15th of the following month.

What about sick leave and parental leave?

EORs manage all statutory leave entitlements: 20–26 days annual vacation (depending on tenure), up to 33 days sick pay per year (14 days for employees over 50), maternity leave up to 37 weeks, paternity leave 14 days, and parental leave 41 weeks.

Is a probation period allowed in Poland?

Yes. Polish law allows a maximum three-month probation period, which EORs include in employment contracts. Notice during probation ranges from 3 days to 2 weeks depending on contract type.

How does an EOR protect IP and personal data?

EOR contracts assign intellectual property rights to the employer company by default. All personal data processing complies with EU GDPR and Polish data protection law, with EU-based data storage.

What happens if I need to end employment?

EORs manage compliant terminations including proper notice periods (2 weeks to 3 months based on tenure) and severance calculations for redundancies. Mutual termination agreements are preferred to minimize legal risk.

When should I switch from EOR to my own entity?

Consider establishing your own Polish entity when you plan to hire 15+ employees, require full IP control, intend to establish a significant physical presence, or are pursuing government incentives requiring local registration.

Sources

- Deel — How to Hire Employees Using an Employer of Record in Poland (2026 Edition) (January 2026)

- Employsome — Employer of Record Market Size & Trends (2026)

- Rise — The 2026 State of Global Hiring: EOR Data, Trends, and Workforce Intelligence (2026)

- Poland Accounting — Labour Law in Poland 2025 (January 2025)

- WageIndicator — Poland Minimum Wage Hike in 2026 (August 2025)

- Mercer — Poland PPK Auto-Enrollment Retirement Savings (2019, updated 2025)

- Bizky — Social Security Contributions in Poland: Employer’s 2025 Guide (2025)

- Skuad — Employer of Record (EOR) Poland | Updated for 2025 (2025)

- Reddit r/eorpeo — 8 Employees in Poland: Time to Ditch EOR? (2025)

- HireBorderless — 10 Best Employer Of Record Services In Poland (2026)

Table of content

- What Is an Employer of Record (EOR) in Poland?

- EOR vs. Entity Setup: A Comprehensive Cost Comparison

- Understanding Poland’s Employer Cost Structure

- The EOR Hiring Process: Step-by-Step

- Compliance Risks and How EOR Mitigates Them

- Key Takeaways

- Frequently Asked Questions

- How fast can I hire an employee in Poland using an EOR?

- What is the minimum wage in Poland for 2025 and 2026?

- Do I need a Polish bank account to pay employees through an EOR?

- What employment contract does an EOR use in Poland?

- Does an EOR manage Polish payroll taxes and social security?

- What about sick leave and parental leave?

- Is a probation period allowed in Poland?

- How does an EOR protect IP and personal data?

- What happens if I need to end employment?

- When should I switch from EOR to my own entity?

- Sources

Related articles

About the Author: Duke Vu